by Emily Hechler

by Emily Hechler

With the cost of college being so high, many students need a student loan. Some expect that a student loan is their fate and don’t think much about it. Others try to use ulterior methods to pay for their college expenses first, and then use a student loan as plan B. While there isn’t a right or wrong way to determine how you will pay for college, you should consider your options before defaulting to a student loan. While student loans can serve as a safety net, they also come with a long-term commitment of repayment that can stretch on for years into the future. Let’s help plan to finance your college experience, whether you use a student loan, other loan, scholarships, or other methods.

How Do I Pay for College Before a Student Loan?

Your first step in determining your best path to pay for college is to fill out the Free Application for Federal Student Aid, or FAFSA. The FAFSA collects information about your and your parents’ checking and savings account balances and federal tax returns. Your parents’ information isn’t needed if you filed your taxes as an independent.

Scholarships and Grants

The results of the FAFSA determine your eligibility for federal and state grants and scholarships. This is free money for you to put directly toward your college tuition. You will have to submit the FAFSA each year, as financial situations change. Depending on how your financial situation has changed, you could receive different funding amounts each year.

In addition to federal and state grants, you can also apply for private grants and scholarships to reduce the cost of college. This can include your high school, college, employer, and other local organizations. These applications might need information from your FAFSA. The FAFSA deadline is usually in June each year, but some scholarship and grant applications might need the information sooner. Pay attention to those deadlines!

Private grants and scholarships can add up and greatly contribute to covering your college expenses. You may be able to cover your expenses for another semester or two because of the amount of scholarship and grant money you’ve been awarded.

Work-Study

Besides scholarships and grants, you may be eligible for a work-study program on your campus. With a work-study job, you’ll receive a paycheck like for any other job. Many students apply their earnings toward their tuition and other expenses to offset how much they will need to borrow with a student loan.

Am I Eligible for a Student Loan?

The results of the FAFSA also impact your eligibility and the amount of money you can borrow through a federal student loan. Money in your checking or savings account is assessed at over three times or a higher rate than the money in your parents’ accounts if they claimed you as a dependent on their taxes, which also impacts how much financial aid you can receive.

A perk of federal student loans is that you don’t have to start paying off your loan balance until after you graduate. This means you can spend your current savings on upcoming tuition costs and not a loan balance. Many students opt for a federal student loan if they qualify over other types of loans because of this benefit.

What are the Different Types of Student Loans?

There are several different types of federal student loans. Your eligibility for any of the loans is based on your FAFSA results.

Direct Subsidized Loan

A Direct Subsidized student loan is available to those who have demonstrated financial need based on the results of the FAFSA. Your college will determine how much of this loan you can take out each year. However, it won’t exceed $5,500. With this loan, the U.S. Department of Education pays toward your interest while you’re enrolled and for a specific period of time after you graduate.

Direct Unsubsidized Loan

A Direct Unsubsidized loan is for students who don’t have financial need based on the results of the FAFSA. Students can borrow up to $20,500 but the amount can vary depending on if they also took out a direct subsidized loan too.

Direct PLUS Loan

If your parents claimed you as a dependent on their taxes, they could borrow with the Direct PLUS Loan. They can take out the amount of their child’s tuition cost minus financial aid that the student accepted. This prevents them from taking out a larger loan with a higher interest rate to help pay for their child’s college expenses.

What Other Loan Options are Available?

Just because you can borrow a certain amount through a federal loan doesn’t mean that you should. You have other loan options! Private student loans are available through third-party organizations. These organizations may use your FAFSA results to determine how much you can borrow. Interest rates and rate terms can vary depending on your situation.

Personal Loan

Alltru offers Personal Loans that you can use for your college expenses. What’s a better place to borrow from than the credit union you already know and love? With a private loan from Alltru, you will start paying toward your balance immediately. This is a great option for those who want to pay off their loan in a shorter period of time.

Special Worker Loan Forgiveness

Teachers can take advantage of Teacher Loan Forgiveness for their Direct Subsidized and Unsubsidized Loans and Subsidized and Unsubsidized Federal Stafford Loans if they have taught for five years in low-income schools.

Government employees, not-for-profit workers, medical workers, and teachers may be eligible for Public Service Loan Forgiveness if they’ve been paying toward their loan for 10 years and meet other criteria.

Home Equity Loan

For adults returning to school after owning a home, your home equity can be used to pay for your expenses. A Home Equity Line of Credit, or HELOC, works like a credit card but with a lower interest rate. This way, you can pay for what you need to borrow as you go to pay off your balance quickly.

How Do I Pay Off My Loan Balance?

If you’re a planner like me, I want to estimate how long it’ll take me to pay off any type of loan balance before committing to it. Even with loans that have set terms, like a car loan, I want to pay it off even faster to save money on interest.

Create a Budget

The most accurate way to estimate how long it’ll take you to pay off your student loan is to make a budget. We have a zero-based budget template for college students to help. In the spreadsheet, you’ll build in saving for future college expenses so you can take out as small of loans as possible.

Consolidate Your Loans

Assuming you borrowed a student loan more than once while in college, you can consolidate them into one larger loan to make payments easier to afford. This allows you to only make one payment a month instead of several smaller payments that keep growing in interest. This loan will have a minimum payment per month, but you can always pay for more than the minimum.

Create a Payment Plan

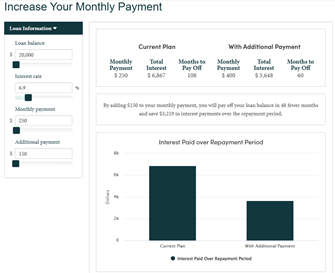

Now that you know the minimum monthly payment, you can use this online calculator to determine how long it’ll take you to pay off your loan balance. Enter your balance, interest rate, and minimum monthly payment. You can also add an additional payment amount to see how much faster you can pay off the loan.

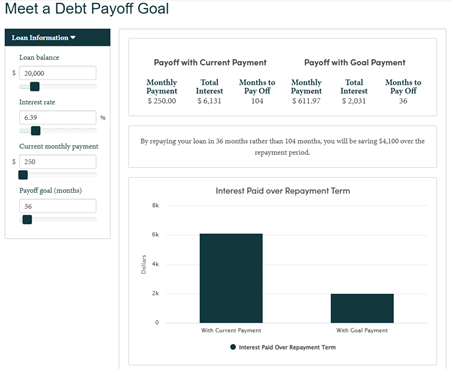

If you’d rather set a timeline goal, you can use the Meet a Debt Payoff Goal calculator to find out how much you need to pay toward your loan balance every month.

Just like finding the perfect college took time, so does finding the best way to pay for your college expenses. Fortunately, student loans are a common way to help you get through your college journey. While you will be paying toward your loan for a while after you graduate, the benefits your college experience offer are often worth the cost. Before you say “yes” to your student loan options, determine how much you really need to borrow. To plan ahead, estimate how long it’ll take you to pay off your loan balance. If you need help determining the best option for you, meet with a Certified Credit Union Financial Counselor at Alltru for help.