by Chelsea Springli

by Chelsea Springli Every couple deals with money in their own unique way. Although it may be a difficult conversation, comparing your spending with your partner’s may be a huge step forward in getting on the same financial page. This is especially true if you’re sharing household expenses, with each partner responsible for specific categories. Being on the same page is key to both partners being able to reach their financial goals, whether they are both contributing to the goal or not. If you’re considering joining your checking and savings accounts, here are tips to make the process easy.

Partner Passwords

The first steps to successfully managing a joint account it to make sure both partners have access to the account. You’ve been warned repeatedly never to share your account passwords, but that rule doesn’t apply with your partner. Each of you must have access to your joint online bank and investment accounts, digital spending trackers, and any other financial apps you and your partner use in managing your money. That doesn’t mean you’re giving up your privacy. However, it is one place where there can’t be any secrets. Honesty about yours and your partner’s financial habits will help you in the long run.

Budget Better

Once you and your partner have access to the joint account, you need to determine together how you’re managing your expenses. You may decide who is responsible for what items in the budget, split bills in half, or whatever method works best for you. No matter which method you use, you are your partner need to create a budget so you are both on the same page about your expectations for managing the account. If you don’t know how to make a budget, here are our top four budgeting methods.

Tracking Tools

If you find keeping accurate track of what you spend challenging, a digital spending tracker might be helpful. Some are websites and some are apps, and they’re free, though some have add-on features designed to provide more options or make them easier to use.

Here are some other apps to check out.

For some people, seeing how much they’re spending on clothing, food and entertainment on a monthly basis is enough to help them slow down the shopping. For others, seeing the dollar amount available for optional spending is all they need to curb their spending desires. And for some couples, the information is enough to make them realize they need to reduce large set costs, which might mean moving to a smaller apartment or leasing a less expensive car.

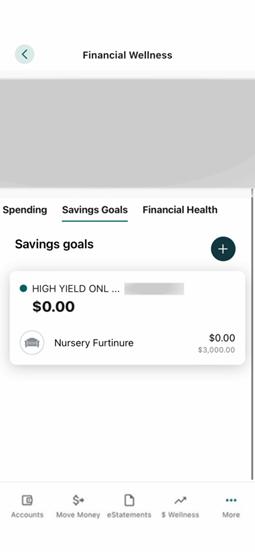

Alltru members can use our free digital banking tools to see their money move in and out of a joint account in real time. Plus, you can set up savings goals connected to your account and receive custom notifications for account transactions.

My husband and I have joint checking and savings accounts. When we first started tracking our spending habits, we quickly realized that I spent more than I budgeted at Home Goods and he spent more than he should have on eating out but came in under budget on personal care items. We wouldn’t have noticed this unless we took the time to monitor our spending from the past few weeks. After you set up your tracking tools, agree to how often you’ll look at your spending together to see how you are holding up your end of the budget.

Monitor Your Money

What happens if one of you, or both of you, are not following the spending plan you agreed on? What’s next? Chances are it means you’re spending more than you had intended to on certain types of expenses. The best first step is to take accountability for overspending. The key to merging accounts is to show that you are trustworthy, even when you mess up. Acknowledging your faults makes space for empathy and growth.

Next, you need to rethink the amounts you’ve allocated to various categories in your budget. For example, transportation costs may be higher than you planned, and there’s no feasible way to reduce them. Can you agree to cut back what you’re spending on something else? Maybe eliminate a subscription package or an upcoming trip or event you planned on attending.

Partnership Pays Off

It’s tough enough keeping track of your own expenses, let alone someone else’s now. So, you shouldn’t be surprised that managing money as a team effort can test your patience, especially if your partner has a different method of keeping financial records. In some ways it’s easier for you today thanks to access to third party and Alltru’s digital banking tools.

Start implementing these joint checking account tips and see what works best for you!