by Emily Hechler

by Emily Hechler

Creating a strong retirement plan means preparing for both predictable and unexpected costs. Many retirees find that expenses like medical care, insurance, and housing take up a large portion of their income. On the other hand, the fun part of retirement like travel and hobbies aren’t prioritized due to financial strain. On top of that, decisions about debt, Social Security timing, and withdrawals from retirement accounts all play a role in shaping long-term financial stability. With a clear understanding of how to budget for your retirement, you can enjoy retirement with an income strategy that works for you.

Retirement Expenses to Save and Budget

Saving for your retirement is only the beginning of the experience. As you approach retirement, it helps to know what expenses to expect so you know how to create a budget. Here is help for planning your expenses during retirement and budgeting to cover the cost.

Debt Payments

Your retirement income won’t be the same as your pre-retirement income. This means that your overall cost of living must be lower too. A major way many accomplish this is by eliminating debt before they retire. A manageable mortgage is the exception to this. You can use a credit card in your retirement, but make sure you can cover your charges every month.

Housing

While you may or may not be paying for a mortgage, you’ll still have to pay for other housing expenses. This includes your HOA, utilities, insurance, and upgrades you undertake. If you move to a retirement community, you’ll have to pay their monthly fees instead. Assisted living and nursing homes can become expensive. By selling your home, you can use its equity to cover the new cost of housing.

Medical Expenses

It’s common to have more doctor’s appointments as we age. You’ll have to cover the cost of copays, prescriptions, and deductibles. You may also need to budget for Part D drug coverage and Medigap or Medicare Advantage costs. Depending on your situation, you may opt for in-home care too.

Insurance

As a retiree, you’ll still pay for your insurance like home, auto, health, life, and more. Many insurance companies charge higher monthly premiums as you age. However, you may be eligible for Medicare once you reach age 65, which can offset some of your medical insurance costs.

Daily Living Expenses

Retirement is so much more than paying for bills, but we still missed a few. Your daily living expenses may change to an extent during your retirement though. Don’t forget to budget for food, lawncare, transportation, clothing, and other household items.

Entertainment

This is the part of retirement that we look forward to. Since you no longer have 40 hours of work a week, you have more time to enjoy entertainment. Common hobbies among American retirees include reading, cooking, gardening, caring for pets, spending time outdoors, traveling, and the arts.

Extra Funds

Like any good budget, you should leave a buffer for unexpected expenses and emergencies. This will help create a cushion, so you don’t have to compromise your daily living or retirement savings. Plus, it also keeps you out of unnecessary credit card debt.

Giving

Many plan their retirement budget below their means so they still have a comfortable amount of money in their savings to give to their kids when they pass. The best way to plan to leave an inheritance is to live debt-free in your retirement. While it’s likely that your debt won’t be passed on to your kids, any debt you owe will be paid from your assets before the assets are given to them. While they’re not inheriting your debt, they’re inheriting less of your savings because of it.

How to Budget for Your Retirement

A zero-based budget is a great budgeting method for retirement. If you need help putting your budget together or managing debt as you balance retirement, talk to a certified financial counselor at Alltru for help.

Retirement Income Planning Guide

Now that you know what costs to expect during retirement, you’re ready to plan for how to pay for them. A retirement income plan is a strategy to give you regular access to as much money possible while keeping your savings intact and growing simultaneously. Here’s what you need to know about creating a retirement income plan.

Plan Your Retirement Age

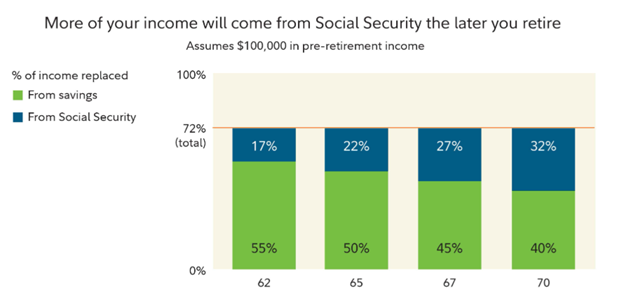

Social Security benefits can begin as early as age 62 for many individuals, but monthly benefit amounts generally increase when benefits are delayed until a later age.

While it’s up to you when you retire, keep in mind that retiring earlier comes with financial consequences. First, you won’t be earning your typical income as long as you may be able to. Second, you won’t get as much money from Social Security. Finally, you’ll have to rely more on your retirement savings to sustain your lifestyle.

Financial professionals often estimate that retirees may need approximately 70–80% of their pre-retirement income to maintain a similar lifestyle, though individual needs vary. This is because it’s assumed that you won’t have high, if any, debt payments during your retirement and you won’t be contributing to your retirement savings anymore. This calculation assumes you will maintain a similar lifestyle in retirement, with spending and expenses close to what you had before retiring.

If you retire at age 62, your retirement savings will need to replace 55% of your income, while the other 17% will come from Social Security. On the other hand, waiting until age 70 to retire only requires your retirement savings to replace 40% of your income, with Social Security covering the other 32%.

Understand Your Retirement Income

In the retirement world, the word “income” is used, even though it’s not the same type as when you were working. Your retirement income is the money you receive each month from your retirement savings plan plus Social Security. Going forward, this is what your retirement income is talking about.

Retirement income comes from a variety of sources, as your retirement plan is funded from different types of accounts. Retirement income is broken into two types, guaranteed retirement income and non-guaranteed retirement income.

Guaranteed Income

Guaranteed retirement income is a source that gives you the same amount of money each month. The money isn’t tied to the market in any way. This makes it dependable for paying your essential bills, like housing, food, and insurance.

There are three main types of guaranteed retirement income.

Social Security

American employees who pay into Social Security, since it’s required, may be eligible to receive Social Security benefits based on their work history and applicable program rules. A perk of Social Security paychecks is that the amount adjusts with inflation. As of 2026, the average Social Security payment is $2,071 a month.

Pension

Pensions aren’t as popular as they used to be. Employers often replace pensions with different plans like a 401(k). Some employers require the employee to contribute to the plan, while others don’t. The amount of money you receive from a pension often depends on your pre-retirement income and length of service with the company. Unlike Social Security, the amount you receive in your paycheck is set for life.

Annuities

An annuity is a contract with an insurance company that may provide a stream of income during retirement. If you choose a fixed-term annuity, you’ll receive your investment back with interest during your payout term. If you choose a lifetime annuity, you’ll receive a payout for the remainder of your life. Depending on the contract terms, annuities may provide a predictable stream of income during retirement. Many annuities also offer survivor benefits, so your spouse can receive the income every month after you pass.

Non-Guaranteed Income

There are several different types of non-guaranteed income. The amount of income you’ll receive from these sources depends on the market.

401(k) or 403(b)

401(k) and 403(b) plan are common retirement plans for employees to pay into today. Many employers offer a match to help you boost your savings. Be mindful that employer contributions may be subject to a vesting schedule. Many choose to roll their 401(k) funds into an IRA as they transition between jobs to keep saving.

IRAs

IRAs, or Individual Retirement Accounts, will be taxed at different times, depending on the type of account. IRAs are individual retirement accounts that are not tied to a specific employer. Alltru offers traditional and Roth IRA accounts to help you meet your savings goals.

Other Investments

Some opt in other types of investments like stocks, bonds, mutual funds, or brokerage accounts. The amount of money you can get back from these accounts varies depending on the market.

Continuing Employment

Even after retiring, some choose to pick up a part-time job to keep themselves busy and to get extra money. If you want a part-time job when you retire, consult with a tax professional, as this increase in income may change how your retirement income is taxed.

Balance Your Income

With so many options and tax implications, it can be hard to determine how much money to withdraw from what accounts at what time. That’s where a certified financial planner comes in. They can help you create a retirement income plan to strategically withdraw guaranteed and non-guaranteed income so you can safely afford to retire.

Review Your Budget

Finally, you should create a budget based on your retirement income plan. This budget should cover your basic needs, then some non-essentials, and finally some buffer in case unexpected situations arise. Check out our blog about what type of expenses to expect in retirement.

If you have any outstanding debt, work with your financial planner to pay off this debt as quickly and safely as possible. High interest rates can quickly eat into your retirement savings.

Getting Started

Now that you understand why you need a retirement income plan, how it works, and how to use it, you’re ready to create one. Alltru works with certified financial planners to help you create a savings plan and withdrawal strategy to fuel your retirement. Schedule your appointment now to start planning.

Retirement Budget Tips

If you’re one of the savvy few who has managed to make it to that coveted plateau that most people strive a lifetime to reach, it’s vital to find strategies that make the most of the money you’ve saved. For many retirees, the fear of running out of money is their greatest worry. They don’t know how to stretch their Social Security benefit to pay all their bills, or they are uncertain about how often, or how much, they can dip into their individual retirement account or other retirement savings.

Check out these four easy steps to stretch your retirement income.

Consider Annuities

After retirement, holding onto what money you have becomes even more important. This means that for most people, this isn’t the time to indulge in high-risk investments. Make an appointment to go over your current portfolio and consider moving any funds wrapped up in risky investments to something safer such as fixed annuities.

Fixed annuities may provide predictable income and protection from market fluctuations, subject to the terms of the contract and the insurer’s claims-paying ability. And if you mix immediate and deferred annuities, you can receive payouts on portions of your money while the rest collects interest. Now that’s making your money work for you.

Next Steps to Consider Annuities

Make an appointment with a financial planner to switch some risky investments to annuities instead to shift from non-guaranteed to guaranteed income.

Reduce Spending

Good advice at any age, this suggestion takes on new importance after retirement. Look to see where you can cut those extra expenses that maybe aren’t so necessary anymore.

This is the time to consider downsizing your home or moving to a less-expensive neighborhood. Most retirees look into traveling with their extra time, so you won’t be home as often. Re-evaluate your in-home perks: TV channels, streaming networks, home deliveries, etc. You might also want to take a second look at life insurance payments. If providing for dependents after your death is no longer a necessity, cutting back on coverage could free up quite a bit of cash.

Next Steps to Reduce Spending

Review your spending history for the past year and see where your money is going. Fill it into a budget. Identity areas where you can cut your spending to keep more of your retirement savings intact.

Trade-Up on Credit Cards

Take a look at the perks offered by your credit card companies and ditch any cards that don’t fit your needs. For instance, if you’re not a frequent flyer, that card that gives you airline miles might not be as beneficial as one that offers cash-back on qualifying purchases.

Alltru’s Rewards Credit Card puts exceptional earning power in the palm of your hand, so you can reward yourself and indulge in your passions. You decide where you want your points to go!

Next Steps for Your Credit Cards

Review the terms of your current credit cards and compare them to credit cards from the credit union. If you carry a credit card balance, you can transfer your balance and get an even lower rate. If you need help, make an appointment with a credit counselor for guidance.

Be a Savvy Consumer

Now is the time to take advantage of off-peak entertainment. Hotels and campgrounds offer lower rates during off-peak times, so does your local golf course, and the movie theater down the street. Taking in matinees, traveling out-of-season, and catching the lunch buffet instead of dinner will all help you stretch your limited retirement budget accordingly. You can also eat dinner during happy hour or even use the perk of using a senior citizen discount. All those things you couldn’t do because of your 9-5 job, now you can do whenever you want. You’ve earned it, so take advantage of all the perks.

Next Steps to Be a Savvy Consumer

Many activities and restaurants offer daytime and senior discounts. Don’t be afraid to plan your schedule around these discounts! Without a 9-5 to report to, you can take advantage of savings on activities you would do anyway.

Stretch Your Retirement Income

Take a serious look at your life and review any changes you can make from your working life. Sure, once you retire, you won’t need a professional wardrobe, and you might not go out for lunch as often. But then again, you might. In fact, the more time you have on your hands, the more likely you are to fill that time with activities that increase spending. So, budgeting properly and being savvy with your newly limited income can help provide additional confidence and financial security.

Downsizing in Retirement

Retiring comes with more free time, more time to think, and more time to plan your dream home! Many retirees choose to move to a smaller home at some point in their retirement, while others use their savings to upgrade. Downsizing may not be as popular as you think. Only 30% of empty nesters downsize in retirement. While you may have a list of reasons why you should or should not move, we put together a list to help you make the decision.

Pros of Downsizing in Retirement

There are many reasons people choose to downsize when they retire. After all, it’s your home, your money, and your life. Retirement is the time to find the home where you want to spend many more hours making memories. Here are some of the pros to downsizing.

Less House to Maintain

As a retiree, you’ll want to spend more of your time enjoying the freedom that comes without having a job. Many retirees prefer spending less time maintaining a large home and more time enjoying retirement. If you choose to live in your current, larger home, there is more space to clean, more faucets to fix, more lightbulbs to switch, you get the idea. A smaller home comes with less space to maintain to make sure your home stays clean, safe, and retains its equity.

Additional Help

By downsizing to a smaller residence, you have several options to live close to help. You may decide to move to a condo or townhouse with an HOA that manages your yard work and snow removal, eliminating the need for you to do the physically demanding chores. You may decide to live in a retirement community with medical staff on-call in case of an emergency. If your children help take care of you, you can move closer to them for faster visits and more frequent visits just for fun.

Senior-Friendly Layout

Navigating stairs, a large layout, or steep driveway can be risky as you age. By downsizing in retirement, you can eliminate these obstacles on your property and look for homes with wider hallways, a shower with a seat, and other options to fit your changing mobility.

Lower Monthly Housing Costs

Downsizing in retirement can save you in your monthly housing costs. If you are still paying off your mortgage, your smaller home may have a lower payment. The area you move may also have lower property taxes and HOA fees. A smaller home is easier to keep cool or warm, reducing the cost of your utility bills. A house with less square footage is less for your insurance to cover, which may reduce your home insurance cost.

Free Up Home Equity

If you’re worried about running low on retirement income, you can tap into your home equity. In this scenario, your current, larger home is mortgage-free. Once you sell the home, you can buy your new one with the equity and profit from the sale and still have some money left to put in savings.

Cons of Downsizing in Retirement

While downsizing in retirement makes sense for some, it doesn’t for all. Even though this list of cons is shorter than the pros, some of the reasons may have more weight than the pros.

Cost of Moving

Selling a large house will likely come with hefty realtor fees and closing costs. This can make a dent on your current finances and may take a while to feel like you’ve recovered with reduced housing costs. Keep in mind that you’ll likely have to pay for movers to help lift and drive your furniture to your new house.

Less Home Equity

By downsizing to a smaller home, your new home is likely worth less than your current home. While this can free up equity in the short term, the value of the home likely won’t increase as much as with the larger house. This may be a concern if you want to use a HELOC or Home Equity Loan with the new house. It also means less home equity to pass along to the next generation, but there may be more in your savings to balance the total.

Less Room for Hosting

This one can be a dealbreaker for extroverts. A perk of a large home is the space to host large groups of friends and family in a convenient location. By downsizing, gatherings like these may be more tricky to navigate. This may be an issue if you have live-in care while hosting out-of-town family members regularly for visits.

Emotional Attachment

Our homes are full of memories. Some families have decades of life milestones tied to their homes like bringing home babies from the hospital, hosting birthday parties, and watching loved ones grow up. For some, they’d rather stay in a large, less convenient house simply because the positive moments outweigh the negative aspects. Sentimental spaces are difficult to say goodbye to. So why do it if you don’t have to?

To Move or Stay Put?

Selling a home and finding a new one takes a lot of work. There isn’t one right answer to deciding to stay in your current home or to downsize. Your decision will be impacted by your health, family, financial situation, and a variety of other factors. Remember to not stress about your decision and enjoy your hard-earned retirement life.

Putting Your Retirement Plan Into Action

A successful retirement budget is built on balance and preparation. By accounting for essential expenses like housing, healthcare, and insurance, alongside lifestyle costs, emergency funds, and personal goals, you can fund all aspects of your retirement.